|

|

What is economics?Economics Definition: the social science that studies the production, distribution, and consumption of goods and services. ScarcityThe earth can only provide a finite amount of resources, we use these resources to produce goods and services. Thus these goods and services are finite. Human needs and wants on the other hand, are infinite. Because the resources used to satisfy these infinite wants and needs are finite, people cannot have everything they desire. Therefor, we can say that the resources the earth provides are scarce. All goods and services that have a price are relatively scarce, this means that even tho they may be abundant, they will not be abundant enough relative to the demand for them. For example, it may seem that cellphones are not scarce, however, you can be sure that not everyone who wants a cellphone has one. This is probably because they cannot afford to buy one, therefor the price of the cellphones is being used to ration the cellphones that are available. Therefor any good or service that has a price is being rationed. Such goods and services are known as economic goods. Opportunity costBecause people cannot have everything they desire, they will need to make a choice. This choice comes at a cost, known as the opportunity cost. The opportunity cost is the cost in terms of a good or service of choosing another good or service. For example, if you decide to buy a computer for $1000 rather than a TV, the opportunity cost of that computer is the TV that you do not get, not the $1000 (opportunity cost is never expressed in money). If a good or service has an opportunity cost, this means that it is relatively scarce, therefor it is known as an economic good. Other things such as air and sea water do not have an opportunity cost, for example, we do not need to give anything up in order to breathe. These things are known as free goods. They are not relatively scarce and therefor do not have a price. The basic economic problemBecause good and services are relatively scare, choices need to be made. These choices can be expressed in three questions that represent the basic economic problem:

Factors of productionThere are four categories of resources that allow an economy to produce goods and services. These are known as the factors of production.

Land

Labour

Capital

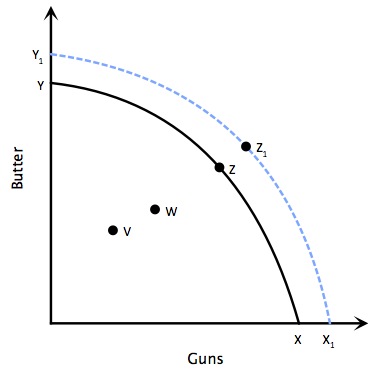

Management Production possibility frontiersProduction possibility curves are used as a graphical method of illustrating choice, opportunity cost and scarcity (as well as other concepts).

Figure 1.1.1 - A production possibility curve Figure 1.1 is an example of a production possibility curve, the only two things produced by the economy and guns and butter. If all production is devoted to producing butter, at point Y, then quantity Y butter will be produced but no guns will be produced. Point X, shows the opposite, only guns are being produced, no butter. At point Z resources are being shared between the production of guns and butter. The points on the curve show the possible combinations of producing guns and butter. It is impossible to produce more guns without producing less butter, therefore the opportunity cost of producing more butter is the number of guns that will no longer be produced. The PPC is a curve because not all the factors of production used to produce one good are equally good at producing the other good. For example, as we move towards point Y, it is unlikely that gun factory workers will be as good at producing butter than guns, therefore there is a smaller amount of goods produced. At point Z, the workers specialized in producing butter are working at the butter factory and the workers specialized in producing guns are working at the gun factory, therefore the production is at it’s most efficient and the total amount of good produced is t it’s maximum. In reality, the actual production is never on the PPC curve as there are always some factors of production that are unused (such as workers, i.e. they are unemployed). Point V represents a combination of actual output. If there were a movement from point V to point W then we would say actual growth has occurred. Point Z1 cannot be aTained by the economy as it is outside of the PPC. The only way to achieve this would be to move the PPC outwards from YX to Y1X1 . An outward shift in the PPC is achieved by increasing the quantity and/or quality of factors of production. If this occurs we say potential growth has occurred since they have the capability to produce more but they are not necessarily using that capability, for actual growth to occur the current point of actual output would need to move towards the PPC. An inward shift in the PPC would mean that there has been a fall in factors of production, this could be due to such things as a natural disaster or war. UtilityUtility is a measure of how much usefulness and pleasure a consumer receives when they consume good or service. There are two different measures of utility: Total utility: The total satisfaction gained from consuming a certain amount of a good or service. For example: If a person eats five slices of pizza, the total utility is the satisfaction gained from consuming all five slices. Marginal utility: The satisfaction gained from consuming one more unit of a good or service. For example: If the person decides to eat a sixth slice of pizza, the marginal utility will be the satisfaction gained from eating that sixth slice. In general, marginal utility becomes smaller with every unit consumed. For example: If a person keeps on eating slices of pizza the pleasure from eating each new slice will be lower, if they continue to eat pizza for too long, they will eventually start felling sick, therefor the marginal utility will become negative as they get dissatisfaction from eating another slice of pizza. Therefor: The marginal utility gained from extra units of a product falls as consumption rises, and may eventually become negative. |

||